Costco: The Perpetual Growth Machine

Nick Sleep's Investment Pitch on Costco

Welcome to issue #005 of Invested Capital. Each week, I share one letter to help you invest smarter, think long-term, and build lasting wealth. My goal? To cut through the noise and bring you timeless lessons from great investors so you can make better decisions with your money and your life. Join 383+ readers learning how to compound capital and wisdom, one issue at a time.

Imagine buying Costco at $45. Today, Costco trades at ~$1,000. A 22-bagger! Many thought Costco was expensive, but Nick Sleep saw something that no one else did: A perpetual growth machine. In this week’s issue, I’m sharing Nick Sleep’s investment pitch on Costco (2005)

Building consumer surplus

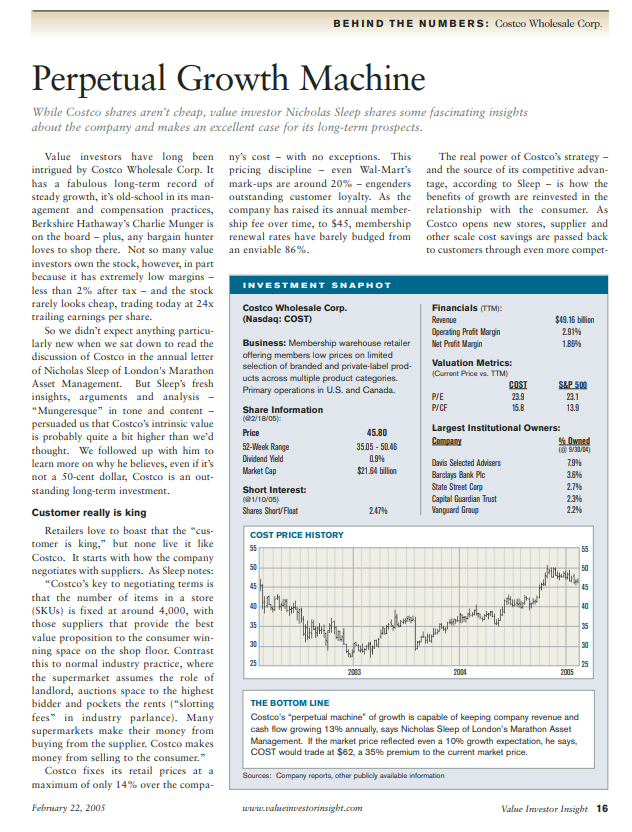

"Costco fixes its retail prices at a maximum of only 14% over the company’s cost – with no exceptions. This pricing discipline – even Wal-Mart’s mark-ups are around 20% – engenders outstanding customer loyalty. As the company has raised its annual membership fee over time, to $45, membership renewal rates have barely budged from an enviable 86%” -Nick Sleep

Building for the long-term

"We often ask companies what they would do with windfall profits, and almost no one replies ‘give it back to customers’. How would that go down with Wall Street? That is why competing with Costco is so hard to do. The firm is not interested in today’s static assessment of performance. It is managing the business to raise the probability of longterm success.” -Nick Sleep

Low margins deter competition

"True, the company has low margins, but that’s the point. The firm is deferring profits today in order to extend the life of the franchise. The firm could earn Wal-Mart margins by taking pricing up a little and the stock would then trade at 11x earnings, but would it be a better business as a result? We think not, because it might allow the competition to catch up.” -Nick Sleep

Low membership penetration

"In Seattle and Alaska, the penetration of membership cards is an astonishing 65% of households, but in most markets it is below 10%.” -Nick Sleep

Stable FCF growth

“Sleep estimates that Costco can conservatively increase revenue and free cash flow by 13% per year into the foreseeable future – 4% from the increasing asset turns of newer stores as they mature, 4% from same-store growth at already-mature stores, and 5% from new stores.”

The Costco flywheel

“This is an early life-cycle company whose competitive moat gets deeper as the company gets bigger and the consumer is consistently cut-in on the benefits of the company’s growth,” terming this cycle a “perpetual machine” of growth.” -Nick Sleep

The thesis

“The consensus has it that Costco is a low-margin retailer with an expensive stock and a cost problem. That is certainly one description. But in our judgment it is a cost-disciplined, intellectually honest, high-product-integrity, perpetual motion machine trading at a discount to value.” -Nick Sleep

Tl;dr

Costco builds for consumer surplus

Costco is focused on the long term

Low margins deter competition

Low membership penetration

Stable FCF growth

The Costco Flywheel: Scaled Economies Shared model

If you enjoyed reading this, the best compliment I could receive would be if you shared it with one person or restacked it

Thanks for reading

Happy Compounding

Matt Harbaugh

Follow me on Twitter/X

Source: