Inside Chris Mayer's 100 Bagger Framework (Every Long-Term Investor Should Know)

What most investors misunderstand about concentration, quality, and how 100x returns actually happen

Welcome to issue #015 of Invested Capital. Each week, I share one letter to help you invest smarter, think long-term, and build lasting wealth. My goal? To cut through the noise and bring you timeless lessons from great investors so you can make better decisions with your money and your life. Join 2556+ readers learning how to compound capital and wisdom, one issue at a time.

Most investors know that the best returns come from holding great businesses for a long time.

The harder question is: how do you actually do it?

How do you sit with a stock for 20 years, through drawdowns, market crashes, and long stretches where your approach looks completely out of step with what’s working, and not flinch?

Chris Mayer has spent his career answering that question.

In this issue, I’m sharing my notes and highlights from a recent interview Chris Mayer did with Drew Cohen and my take on the principles of his approach.

By the end of this newsletter, you’ll understand:

Why concentration and quality are inseparable

Why margin of safety is not just the price you pay, but the quality of the business you own

Why a premium multiple isn’t automatically a warning sign

How deep research builds conviction that keeps you invested through the inevitable drawdowns

Why reducing the number of decisions you make can help you avoid mistakes

Let’s dive in.

Chris Mayer’s Investment Philosophy

“Businesses that have high returns on capital, lots of reinvestment opportunities, there’s skin in the game, great balance sheets. Aim to own them for as long time. I avoid leverage, try to avoid things that are overtly cyclical. It’s global, so I go everywhere, fairly concentrated. I have 12 stocks today.” -Chris Mayer

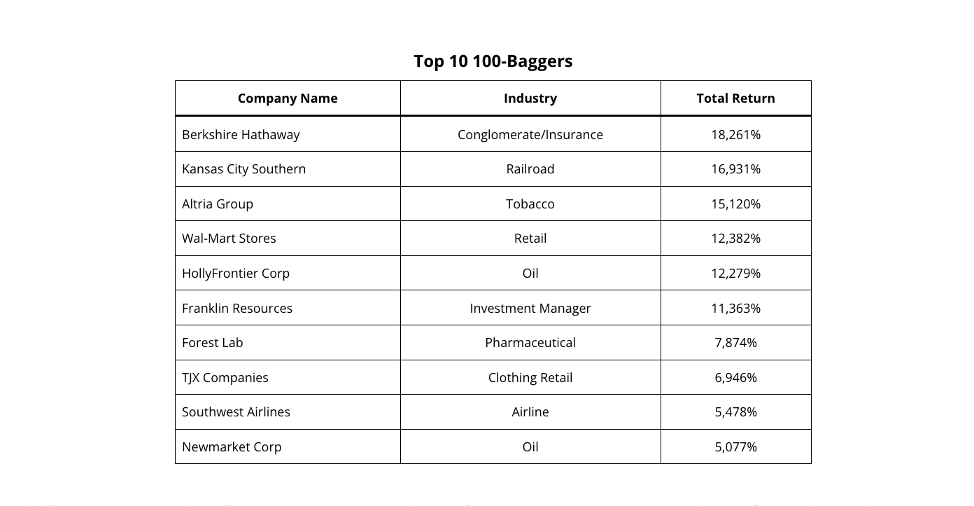

To give you an idea of who Chris Mayer is, Chris wrote the book 100 Baggers: Stocks That Return 100-to-1 and How to Find Them.

The book is centered on the idea of how to find young quality-growth companies that can be a 100x in 20-25 years.

If you read this book, you can get an idea of how Chris Mayer invests because many of the characteristics that he lays out in that book are what he looks for in an investment and how he manages his portfolio.

He focuses on businesses that have

High ROIC

Lots of reinvestment opportunities

Management is aligned with shareholders with large equity stakes

Great balance sheets that have a net cash position

Have predictable earnings and cash flows

Be Concentrated

“I’m focused on that sort of internal engine of compounding… and being concentrated changes what you can invest in. You can’t invest in things that have a lot of leverage or some existential threat to be a zero anytime soon. So you’re kind of narrowing the universe a lot that way when you’re that concentrated.” -Chris Mayer

Usually, when investors are looking at opportunities with higher potential returns, that tends to come alongside more diversification.

An example would be a venture capital investor where they would have a huge portfolio and they expect 90% of them to fail, but the other 10% do really well.

In the same way, Chris Mayer is looking for companies that grow 100x, but he differs in that he is concentrated.

Chris states that most of the 100x baggers he studied it takes 20-25 years to reach that milestone.

In contrast to a VC investor, where they are looking to get those types of returns sooner, Chris Mayer is willing to wait longer and be more “focused more on the internal engine of compounding.”

In short, he has more confidence in the companies he owns and there’s a shorter left tail probability distribution where there’s not a big bankruptcy risk for example.

And when you are concentrated, it narrows your investable universe.

When your investable universe is narrow, you can spend more time researching and building up your conviction.

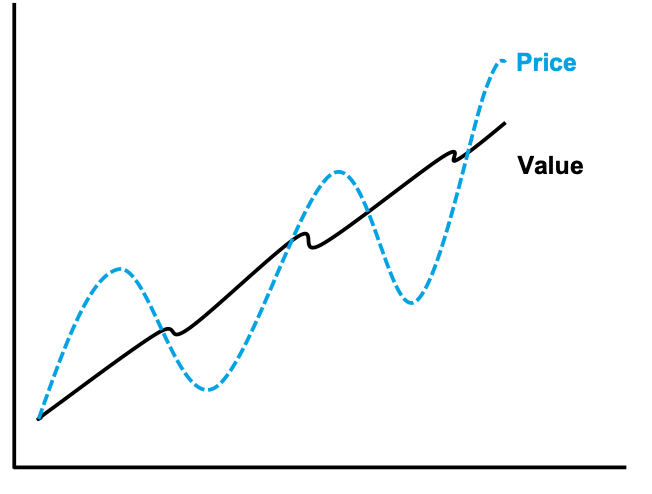

Margin of Safety Comes From the Quality of the Business and the Price You Pay

“Margin of safety comes primarily from the quality of the business with a combination of a good entry price.” -Chris Mayer

Ben Graham has taught value investors that your margin of safety comes from the price you pay.

This typically looks like buying a stock 30-50% off your estimate of intrinsic value.

However, this is only one side of the story.

The other side comes from the quality of the businesses you own.

Chris Mayer states that, in his 100 baggers study, drawdowns are inevitable.

Berkshire Hathaway was the best performing in that study and got cut in half at least 3 times.

Which means that “margin of safety doesn’t mean that the price doesn’t go down but it means that the business is not going to be impaired.”

The margin of safety comes from having a higher confidence in a company’s ability to compound.

Chris Mayer spends a lot of time studying the competitive advantage of the business and the industry to help increase his confidence and thus his margin of safety.

So when you are thinking about your margin of safety in an investment, focus on the price you pay and the quality of the asset you are about to own.

Premium Multiples Don’t Always Mean Risk

“These companies will hold their multiple for a long time, so it’s not like it trades at a premium multiple and that goes away. A lot of times these businesses carry a premium multiple for years and years, decades above the market premium. And over a long enough period of time, the importance of that multiple, it doesn’t go away entirely, but it starts to shrink over time.” -Chris Mayer

Looking at a higher P/E or P/FCF multiple in isolation can be a mistake.

Just like a deep-value stock that’s trading 5x earnings, and there’s a reason why it’s trading at that multiple, there’s a reason why some businesses tend to hold premium multiples.

While paying a high multiple for a stock is risky for you as an investor in isolation, you have to take into account the quality of the business, what the organic growth rate is, and what the reinvestment rate is.

If the business has durable competitive advantages and can sustain its growth rates, that business will grow into that high multiple, and the importance of that multiple fades away.

“If you have a business that compounding at 20% a year, after a decade it's like a 6x increase in cashflow, so it doesn’t matter that much you pay 20 times or 25 times.” -Chris Mayer

This reminds me of the chart Terry Smith has shown of P/E multiples you could have paid and still had a 7% return.

In his book Investing for Growth, Terry Smith states that you could have paid 281x earnings for L’Oreal in 1973 and beaten the index return.

“Growth can enhance or diminish the value of a company- growing a business with inadequate returns is simply sending good money after bad. But when a company has superior returns on capital employed, and a source of growth which enables it to reinvest a substantial portion of those returns, the result is compound growth in its value and share price over time.” -Terry Smith

Yes, many of these “quality” companies trade at a premium multiple, and only looking at that premium multiple in isolation can be a mistake because you need to understand 3 things: 1) how fast the company is growing, 2) why it’s growing, and 3) how long that growth can last (durability).

A high multiple only makes sense if the underlying growth justifies it.

As Chris Mayer states, “focus more on the internal engine of compounding.”

Reduce the Number of Decisions You Need to Make to Avoid Mistakes

“When you cut back on the number of decisions you need to make, you’re cutting back on the potential to make a lot of mistakes.” -Chris Mayer

When asked whether he would sell a company when it gets ahead of itself in terms of valuation, Chris Mayer states that making that sell decision regularly across your whole portfolio creates a lot of challenges and that he stays on the side of letting them ride, rather than constantly buying and selling.

The reason why is that selling increases reinvestment risk because your next idea has to be better than the idea you have.

“What are the odds that you’re going to get them right. We assume that we’re going to get them right but you’re going to get some of those wrong and you may get some right and then you reinvest the capital elsewhere and get that wrong. There’s also a tax drag also. So you sell an idea, you take a tax hit on that, your next idea has to be quite a bit better than the idea you have. You have to play around with some sort of odds on how often you’re going to be right. If you’re at 50/50, it’s not worth, you have to get right a certain percentage of the time and then your reinvestment risk, you have to get that right.” -Chris Mayer

When you cut back on the number of selling decisions you need to make, you’re “cutting back on the potential to make a lot of mistakes.”

But Chris Mayer also notes that it all comes to personal preference.

What risk are you willing to live with?

Are you more willing to live with the fact that you’re going to get rid of companies when the multiples expand a little outside of your comfort zone and you’re okay with leaving money on the table, or are you willing to go ahead and take the risk of continuing to own it, but possibly suffer a drawdown later when a multiple comes in?

There’s no real answer.

It’s how you want to play the game, what your goal is, and what your skill set is.

Just remember that when you sell a position, it does increase reinvestment risk, and when you reduce the number of decisions you need to make, you can avoid mistakes.

How to Find 100 Baggers

“It’s not really systematic, it’s a lot of reading, a lot of talking to people. You find these adjacent ideas and just keep exploring and that’s how you find them, and then I do try to get to know them very well.” -Chris Mayer

How Chris Mayer finds his ideas is not systematic.

It is by reading a lot, talking to other investors, reading other investors’ letters, and exploring adjacent ideas.

How he found out about Roco was that he was invested in Lifco and wanted to know where the previous CEO went and found out that the previous CEO started this business called ROCO.

When he finds an idea he likes, he wants to know them well.

It depends on the company but he also likes to talk to management as well, because they can explain some things about the business which helps him gain more clarity in how the business works.

Research Builds Conviction

“The main reason we do all this research is to build up our own conviction, you increase the odds that perhaps down the road that you’ll make the right decision because a lot of things happen, you’ll get news and if you know it really well, you’ll know how to correctly interpret it that news and you’ll react differently that someone who doesn’t know it as well.” -Chris Mayer

When you manage other people’s money, you have to have a high hurdle and have a high understanding of the business before starting a small starter position.

“You learn a lot when you own something than when you’re just following it. You’re learning different things that you maybe don’t appreciate as much when you don’t own it and you were just looking at it from the outside.” -Chris Mayer

Researching a business and understanding it thoroughly allows you to gain confidence in you investment assumptions, which allows you to have more certainty in the range of potential outcomes for that investment.

If we inverse this, an investor who doesn’t do the research and know the business inside and out, when the stock falls 10 or 20%, they are going to freak out and sell out.

Their turnover is going to be way higher for that novice investor’s portfolio, and their returns will be lower compared to an investor who can understand a business and stay in the game when events occur.

As Chris Mayer states in the interview, these 100 baggers take a long time, 20-25 years for them to reach that status.

And throughout those 20-25 years, there will be drawdowns.

That is inevitable.

Berkshire Hathaway, for example, fell 50% at least three times.

I am reminded of this 2009 interview, where the reporter asked Charlie Munger, “How worried are you by the 50% decline in the Berkshire Hathaway share?”

And Charlie’s response was spot on:

“Zero. This is the 3rd time that Warren and I have seen our holdings in Berkshire go down top tick to bottom tick by 50%. I think it’s in the nature of long term shareholding, with the normal viscitudes and worldly outcomes and markets that the long term shareholder has his quoted value of his stock go down by 50%. You can argue that if you’re not willing to react with equanimity to a market price decline of fifty percent two or three times a century, you’re not fit to be a common shareholder and you deserve the mediocre result that you’re going to get.” -Charlie Munger

This ties into our point on margin of safety and investing in a great business.

You can increase your margin of safety by understanding the business more and more.

As Warren Buffett once said:

"Risk comes from not knowing what you’re doing.” -Warren Buffett

Peter Lynch would also say, “Know what you own, and know why you own it.”

Frederick Kobrick, the author of the book The Big Money, also had this to say on why research is critical in building conviction:

“Naturally, because markets and stocks have volatility, knowledge is a great asset to have. Knowledge brings confidence, and confidence is what keeps people in stocks that are undergoing price pressures yet continue to have great growth in earnings.

Confidence is what helps successful investors to buy more shares when prices dip, while investors who do not know what they own become emotional and sell out of fear and lack of knowledge.”

-Frederick Kobrick, The Big Money

This is all to say that the research you do is extremely important, as this will help you build your conviction in a stock, improve your margin of safety, and allow you to act more rationally in extreme events, such as a recession.

Being a Good Seller is the Hardest Task in Investing

“Most of the time the sell decision comes down to company speficic things but it can also be other things going on in the portfolio. You have more attractive opportuntities. You have to have confidence when you are investing in something new. But you balance the confidence with recognition that you could be wrong.” -Chris Mayer

“Being a good seller is probably the hardest thing in investing.”

When Chris sells a position, most of the time the bar is higher because these businesses are higher quality, and most of them, if you stick with them, eventually will go up in price.

It never feels good to sell.

How Chris determines to sell a position comes down to company-specific things, but it also comes down to what else is going on in your portfolio.

You may have other attractrive opportunites that the opportunity cost of holding a position in X is higher than buying a new position in Y.

As we mentioned in reducing the number of mistakes you want to make, selling can increase your reinvestment risk, so you have to have confidence when you are investing in something new, you balance the confidence with recognition that you could be wrong.

Pay Tuition Early

“The greatest investing lessons you will learn are not the ones you read in a book but the ones you experience yourself. It helps to make a lot of mistakes when you are young and don’t have a lot of money so that you don’t repeat those same mistakes when you are older and have a lot of money.” -Chris Mayer

The most powerful investment lessons you will learn are the mistakes you make in the beginning of your investing journey.

Over time, these lessons will shape you and how you invest, which will help prevent you from making the same mistakes later in life when you have a lot of money.

It’s better to learn and make mistakes and find your investment philosophy sooner rather than later, so you don’t make those mistakes in the future, because a 50% mistake on $1,000 is only $500, whereas a 50% on $1 million is a $500,000 mistake.

Don’t Follow Superinvestors

“You can’t borrow conviction from superinvestors like Stanley Druckenmiller because they change their mind multiple times and there have been many cases where these smart investors are involved big blow ups.”-Chris Mayer

Don’t blindly invest in a stock just because your favorite super investor does.

There were many investors who followed Charlie Munger in his Alibaba investment in 2021 blindly, and only invested because Munger bought the stock.

You can’t borrow conviction.

You can get ideas from these investors to research more, but you can’t outsource your thinking to them.

When they sell out of it the next quarter or so, you will likely sell out as well, thinking, “If they’re selling, they must know something I don’t.”

Micron is getting a lot of air coverage at the moment as it has rallied up to a $1 trillion market cap.

Mohnish Pabrai and Li Lu had decent weightings in the name (Micron made up of 80% of Pabrai Funds), but in 2Q23, they both sold out.

I know some investors invested in Micron only because they saw Mohnish Pabrai and Li Lu buying and holding it, but when they sold, I would bet many of those investors followed suit and sold as well.

Hindsight in 20/20, but that would have been a costly mistake, as from that period in 2Q23 to today, you would have a 10-bagger if you understood the business inside and out and not have borrowed your conviction.

Don’t Be Afraid to Look Like a Fool

“There are definitely going to be stretches where you look like a fool, and if you’re not comfortable with that, then investing is going to be tough for you.” -Chris Mayer

The market is unpredictable and there are periods where some investing styles go in and out of favor.

For example, many “quality compounders” are in a sell-off, and investors who are more quality-oriented (myself included) have not performed as well as someone invested more in mega-cap tech and semiconductors.

Or if you are a software investor, it looks foolish to invest in this space after the 30-50% sell-offs we experienced earlier this year.

As I have mentioned in the last issue, Aswath Damodaran: How to Find Your Investment Philosophy, there is more than one way to invest, and you need to find an investment philosophy that is authentic to you, so when you go through stretches where you are underperforming and “looking like a fool”, you don’t style drift.

You stay the course because you are comfortable with how you are investing.

When you do this, you can make more rational decisions.

Don’t be afraid to look like a fool.

Tl;dr

Concentration narrows your investable universe

Margin of safety comes from the price you pay and the quality of the business you own

A premium multiple isn’t always risky

Reduce the number of decisions you need to make to avoid mistakes

Read a lot and talk to other investors to find potential 100 baggers

Research builds conviction

Being a good seller is the hardest thing in investing

Pay tuition early

Don’t blindly copy superinvestors

Don’t be afraid to look like a fool

If you enjoyed reading this, the best compliment I could receive would be if you shared it with one person or restacked it

Thanks for reading

Happy Compounding

Matt Harbaugh

Follow me on Twitter/X

Source:

Finding Quality Compounding Stocks: Chris Mayer Interview with Drew Cohen (2026)

Great job as always.

Nice post!